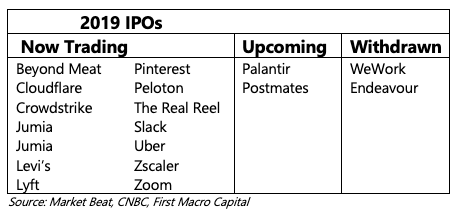

This year’s recent batch of IPOs like Uber, Lyft, and Slack, Zoom, Smile Direct, Pinterest saw much of their explosive growth captured during their private markets phase. Leaving much less growth upside available to public investors. How much growth is now truly available now that they are publicly traded companies, particularly as we near the end of the business cycle?

Templeton, said this about the 2000 tech bubble:

One of the most successful investors the world has ever seen, the late John

“This is the only time in my 88 years when I saw technology stocks go to 100 times earnings; or, when there were no earnings, 20 times sales,” says Templeton. “It was insane, and I took advantage of the temporary insanity.” (Forbes)

What he did next:

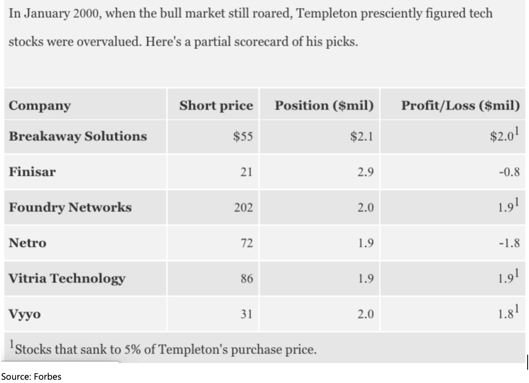

He shorted 84 Nasdaq stocks, taking positions averaging $2.2 million each. In nearly half of the shorts he waited until prices dropped to 5% of what he paid, thereby cleaning up on such names as Foundry Networks, Breakaway Solutions and Vitria Technology (see table, above). At other times he closed out his positions once the stock price dipped below 30 times trailing earnings. He took losses early, quickly covering positions where the stock price increased post-lockup.

Templeton slated his short positions to take effect 11 days before lockup expirations—that point, usually six months after an initial public offering, when insiders are allowed to sell their stock. He focused on tech shares selling at three times the price set in the initial offering, rightly figuring company insiders would cash out some of their absurdly valued holdings, putting downward pressure on stock he suspected was due to fall anyway. “Insider selling was the trigger but not the main driving force,” he says.

The early-2000 overpricing of Nasdaq is what they call a once-in-a-lifetime opportunity. Templeton doesn’t think it will recur in his life.

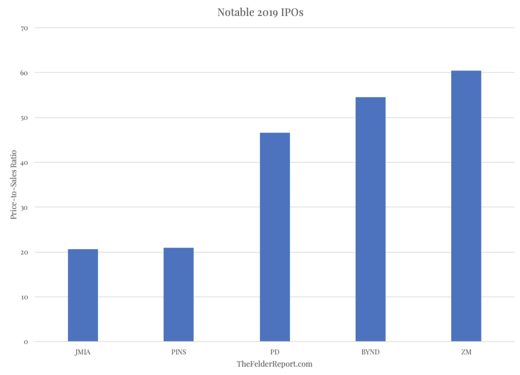

The similarities of this year’s tech “unicorns” IPOs today have all the same of the tech bubble of 2000. No earnings and 20 times sales at IPO. It took less than 20 years for the tech euphoria to occur all over again. Some of these companies will be wonderful to own when the prices fall down, and some may never see their IPO highs again.

Then in this cycle, we saw the Smile Direct Club IPO do what no IPO has done since the top of 2008, to raise more than $1 billion and still sink from its IPO price.

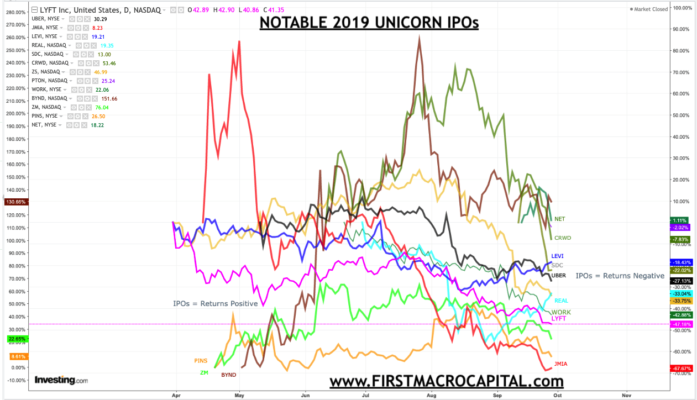

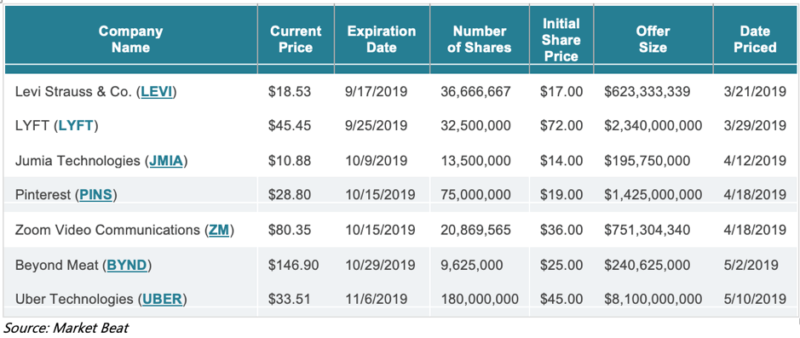

Here is a look at the returns of some of the recent IPOs, where there is probably more pain coming because we have only recent seen the US manufacturing sector turn negative.

IPO WARNING SIGN

What happens when the second batch of IPOs go public? What are investors going to sell to buy these new IPOs? Will investors even participate after getting burned from the first batch? Is the SmileDirect Club IPO flashing a warning sign? We are seeing it with the WeWork IPO.

Lockup Time is Coming

Then there is the lockup expiration of shares that will put pressure on their share prices, with Levi’s the first one to hit the share lockup expiry date. This could lead to selling pressures in the stock market, particularly in October during an already have news cycle because of earnings, the Fed, and trade.

If It Can Happen to Amazon – It Can Happen to Them

The public markets are quickly giving these new IPOs a reality check, and as the tech bubble slows if we look at Amazon which is now one of the largest companies in the world, worth $1 trillion dollars, fell by more than 90% at the end of the tech bubble. The question remains will history repeat?

Disclaimer:

The information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your financial situation – we are not investment advisors, nor do we give personalized investment advice. The opinions expressed herein are those of the publisher and are subject to change without notice. It may become outdated, and there is no obligation to update any such information.

Investments recommended in our publications, blog posts, emails, online communications, or any online contents published by any party of First Macro Capital and its affiliated companies should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company in question. You should not make any decision based solely on what you read here.

First Macro Capital writers and publications do not take compensation in any form for covering those securities or commodities. First Macro Capital employees and agents of First Macro Capital and its affiliated companies own some of the stocks mentioned in this article, prior to the writing of this article.

Get the exact checklist that Professionals use to find winning Gold mining producer stocks.

Apply this to any mining producer stock in under 30 minutes!